What should or should not be in your safe deposit box? With the rise of electronic storage, demand for safe depot boxes has fallen, causing some banks to eliminate their safe deposit box operations.

By Emily Kampeter, Vice President & Wealth Management Advisor

You know your kids and grandkids prefer texting, so you oblige. You send a text about some estate and financial planning changes you’re exploring. One child replies with TLDR. It means Too Long; Didn’t Read. Don’t be discouraged by every acronym or hashtag (you may know it as a pound (#) sign) used by the next generation. We can help you understand their values, how to approach them about future wealth planning, and the latest money trends they’re following.

Millennials | Born between 1981-2000 | Ages 24 to 43

Millennials value challenges, growth and development, work/life balance and prefer a fun work environment. Their lives were shaped by a global financial crisis and climate change. They give to children’s causes and on average contribute to three charities annually.

Gen Z | Born between 2001-2020 | Younger than age 23

Gen Z values diversity, creativity, technology and personalization. Their lives were shaped by access to the internet and technology growth, COVID-19, unaffordable higher education and political unrest. They care about the planet, social causes, data-driven results and volunteering.

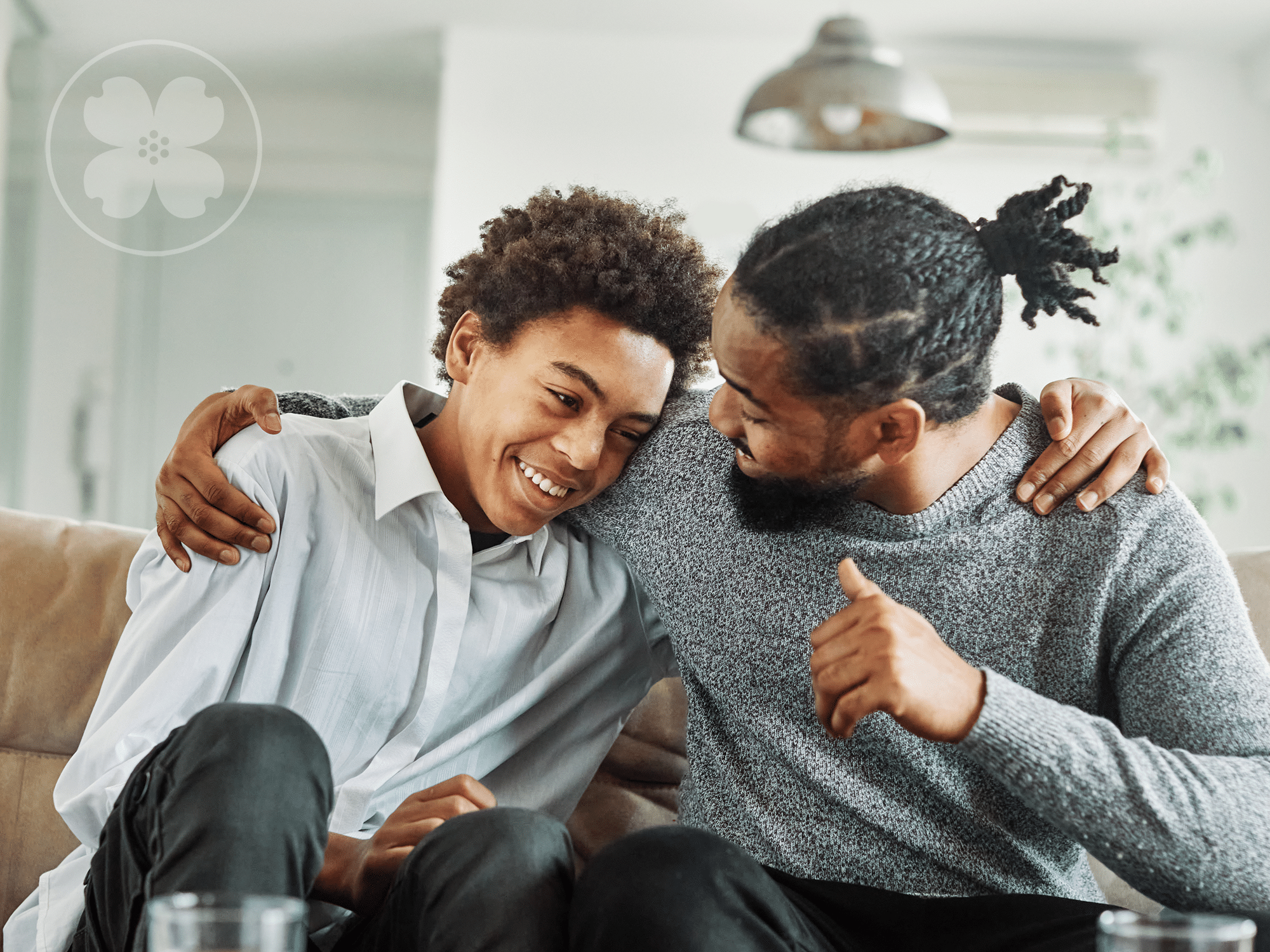

Family Meeting

Both generations demand quality digital experiences, but when it comes to difficult decisions, they want human interaction and personal expertise. Finally, something you can all agree on. Rather than sending texts, set up family meetings to talk about the future. They can be in-person or online. The purpose of these meetings is to reduce stress, increase financial education and prepare the next generation for what’s ahead.

Terms to know:

- FIRE (Financial Independence, Retire Early) – A movement devoted to extreme savings (up to 70% of annual income) and frugality to retire early.

- YOLO (You Only Live Once) – A mindset that values experiences over possessions. For example, “I’m going to spend $400 on a concert because I only live once.”

- FOMO (Fear of Missing Out) – Some people make purchases outside their budget or decide to invest in something because everyone else is doing it. Unfortunately, these decisions are based on emotion or fear rather than facts.

- Soft Life – A lifestyle that embraces low stress and mental wellness by using more money in the present rather than in the future. It challenges the traditional idea of working hard, savings money and retiring early.

- #girlmath – Girl math describes how some people justify their spending habits. For example, if you pay with cash, it’s free because the balance in your account doesn’t go down. If it is on sale, you’re making a profit because if something cost $50 and you pay $30, you make $20. Of course, the math may not add up.

- Cash Stuffing – Setting aside cash in envelopes for each spending category at the beginning of each month. A simple practice is to put 50% aside for needs, 30% for wants and 20% for savings.

- Loud Budgeting – A technique of declining social activities when it puts your financial goals at risk. It encourages people to be vocal and proud about their decisions.

Central Trust Company can help you plan, design and conduct family meetings. We can also help answer questions and support your efforts in a way that makes sense for you.

Related Articles